As much as the family office industry has boomed over the past 10 years, certain myths about it pervade. Sometimes these myths overstate, understate, or cloud the perception of what is or what is not a family office. Types of family offices vary dramatically; what is critical to consider are the services tailored to the family office based on what the family actually “needs” versus what they “want,” as well as what the family can afford. To follow are three common family office myths as described in The Wealth of Wisdom Podcast with contributing author, Kirby Rosplock, PhD who spoke about this topic in her chapter, “Should You Choose a Single-Family Office or a Multi-Family Office?”1

Myth 1: With great financial wealth and power, there comes a need for a robust, full-service family office.

Many people believe that families of great wealth require a family office with all the bells and whistles. The reality is that some families will opt to build an outsourced, virtual type family office structure preferring not to build another major enterprise. Many founder family office type structures have simple organizational charts, including a president, bookkeeper, and administrator. In the commercial wealth management space, there is an incredible network of providers, partners, and institutions that can be leveraged relieving the office from building an enormous, complex, internal structure. For some families, it is attractive to have access to top talent through these providers, yet not have to worry about human resources considerations such as payroll, incentives, short-term and long-term compensation, and benefits.

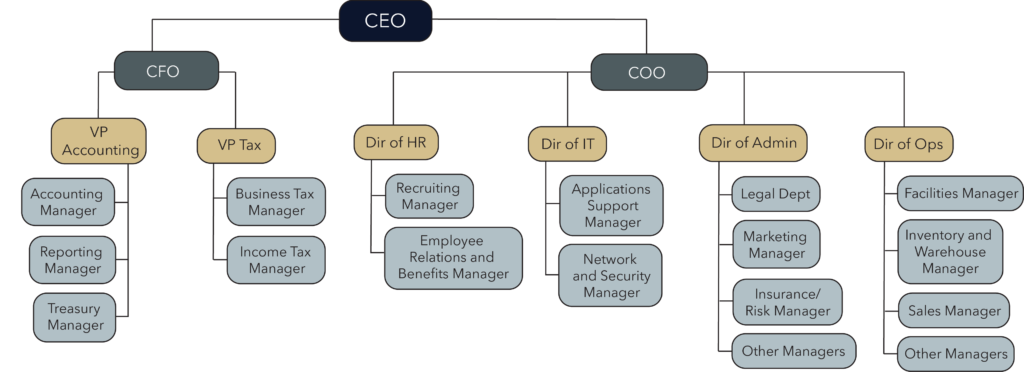

Slide to view the difference between a simple family office organizational chart and complex family office organizational chart.

.png)

Myth 2: Family members should be the operators of their family office.

Although it is common for family, particularly wealth creators, to assume a leadership role in a family office, it is less common in second and third generation family offices that a family member is in a leadership role. In fact, many would argue that having professional managers who are detached and objective as well as trained in the technical disciplines of finance, investing, tax, compliance, estate planning, accounting, business management, among other areas, may be better stewards to serve in leadership roles than family. When families are placed in a leadership role who have not necessarily earned it, concerns of nepotism may encroach into the culture of the office. Sometimes it makes more sense to look at each family member’s talents and put them to best use by applying them strategically. When families figure out the capacities in which each family member best performs, they can most effectively apply their skills. Then they can look at what their ownership and business needs are and hire the best people for those positions to ultimately serve the goals of the overall enterprise. If attracting family members into leadership roles is desired, it’s recommended that onramps be crafted with purpose-driven leadership development plans, goals, and milestones as a means for demonstrating competence, capabilities, training, and experience before stepping into leadership roles.

Myth 3: Family offices only manage a family’s financial wealth.

In its best form, the family office provides a structure that helps preserve the family enterprise by supporting four dimensions of the family:

- Business legacy, where wealth originates

- Financial legacy, where financial security of wealth is maintained

- Family legacy, where family comes from and is headed in the future

- Philanthropic legacy, where the family gives back to the community2

There are many different single family office archetypes. Although managing wealth is a huge part of any family office, family offices also provide lifestyle planning, investment advice, tax compliance, estate planning, wealth transfer planning, document storage, risk management, governance, financial education, and philanthropic services. Family offices are built to exist longer than the tenure of one generation, so spending time planning and communicating a family’s values, mission and vision is crucial for the longevity of the family office.

Moreover, family offices are expected to provide education and training with each new generation rising up within the family. Preparing, developing, and inspiring the rising generation is important for sustaining family wealth. Yet often, being a great teacher, mentor, coach, and guide is not written into the job description of most family office executives. Further, it is a major undertaking to translate complex information into digestible, age-appropriate learning content that is right-sized for different family groups and audiences. So, family wealth education is still a complex area for many family offices to manage.

Although family offices and their structure, service offering, and organizational chart do not need to be as complicated as the family it serves, they can be just as diverse. There is no right or wrong way to approach the design of a family office. Most importantly, families need to understand and explore what their vision, mission, and goals are in order to build a lasting family office and over time adapt their family offices to their evolving needs.

McCullough, Tom, host. “Should You Choose a Single-Family Office or a Multi-Family Office?,” by Kirby Rosplock, PhD. Wealth of Wisdom Podcast, Episode 17, 2019, https://wealthofwisdombook.com/podcast/

Rosplock, Kirby, The Complete Family Office Handbook. Wiley, 2014.